Step-by-Step Guide to Buying Your First Home: Everything You Need to Know

Step-by-Step Guide to Buying Your First Home: Everything You Need to Know

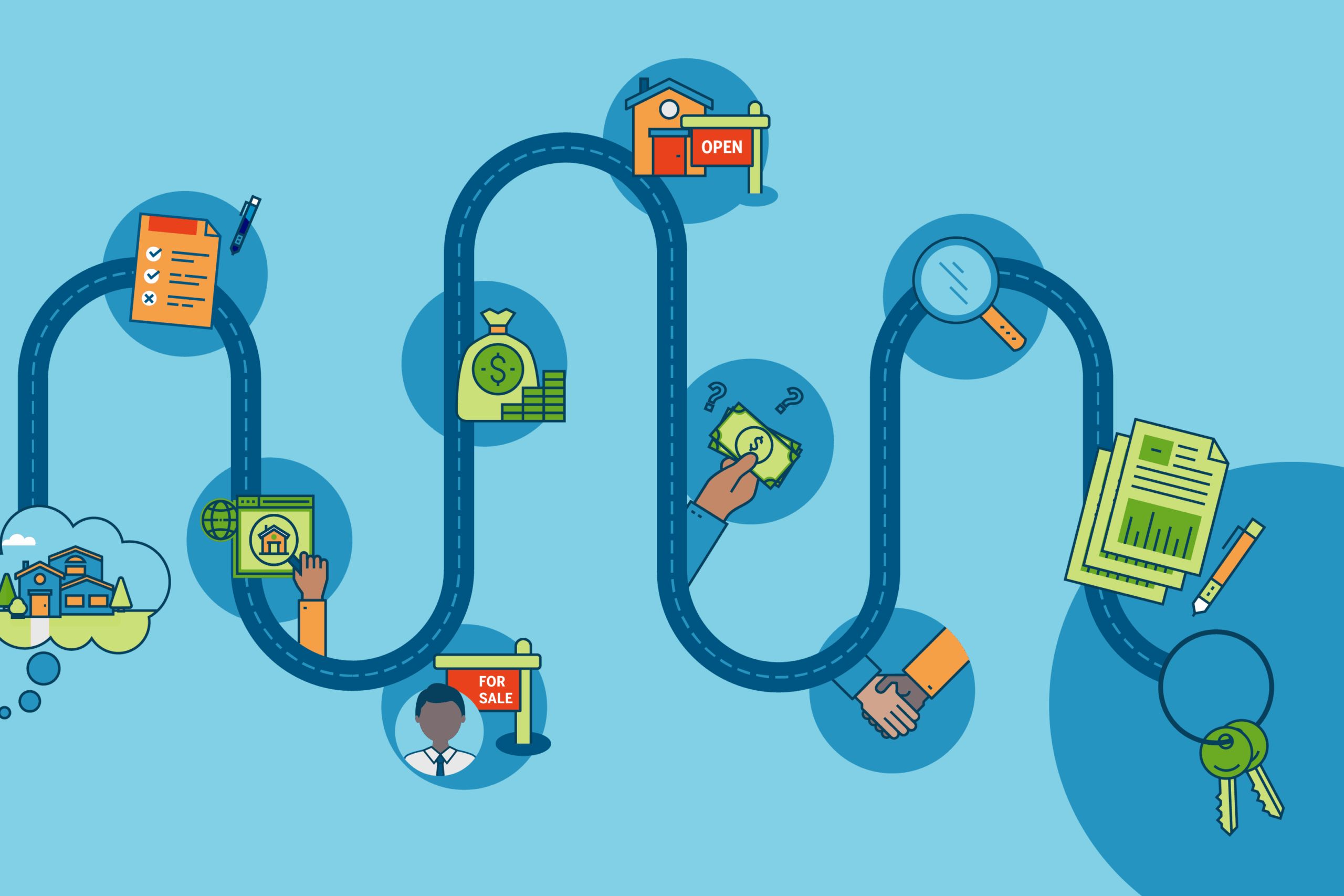

Buying your first home is one of the most significant milestones in life, but the process can feel overwhelming without the right guidance. From saving for a down payment to closing the deal, every stage requires careful planning, research, and smart decision-making.

This guide provides a detailed step-by-step breakdown of the homebuying journey, explores the benefits of using modern technology to simplify the process, and offers real-world examples to help you understand what to expect as a first-time homebuyer.

Why Buying Your First Home Is a Big Milestone

A first home is not just a place to live; it’s an investment in your future. For many people, it represents financial independence, stability, and personal achievement. Unlike renting, owning a home builds equity, gives you freedom to customize your space, and provides a sense of permanence.

However, navigating the real estate market can be intimidating. Mortgage terms, property searches, and legal requirements can feel like uncharted territory. That’s why understanding each step beforehand is crucial to avoid costly mistakes and make informed choices.

A Young Couple Reviewing a Mortgage Pre-Approval Letter

This image highlights the financial starting point of the homebuying process — knowing your budget and mortgage eligibility.

Relevance: Pre-approval sets realistic expectations and helps first-time buyers narrow down suitable homes.

Step 1: Assess Your Financial Readiness

The first step in buying your first home is understanding your financial situation. Lenders look at factors like your credit score, income, debt-to-income ratio, and savings for a down payment.

Creating a clear budget ensures you know how much house you can afford without straining your lifestyle. Remember to factor in hidden costs like property taxes, homeowner’s insurance, maintenance, and closing fees.

Being financially prepared helps you avoid surprises later in the process and increases your chances of loan approval.

Step 2: Get Pre-Approved for a Mortgage

Pre-approval is a critical step that demonstrates to sellers and real estate agents that you are a serious buyer. It involves submitting financial documents to a lender, who then confirms how much they are willing to lend you.

A pre-approval letter not only gives you a spending limit but also strengthens your negotiating position when making offers. Without it, sellers may not take your interest seriously.

Step 3: Define Your Home Needs and Wants

Before starting your search, list the must-have features for your home and the “nice-to-have” extras. Consider location, size, number of bedrooms, proximity to work or schools, and lifestyle needs.

Separating needs from wants helps you stay realistic within your budget and prevents emotional decisions. A clear checklist also makes the search process more efficient when working with real estate agents.

Step 4: Work with a Real Estate Agent

A knowledgeable real estate agent can make the buying process significantly easier. They provide insights into market trends, help identify suitable properties, and negotiate on your behalf.

For first-time buyers, an agent is especially valuable because they explain unfamiliar terms, guide you through paperwork, and ensure you’re not overpaying for your home.

Real Estate Agent Showing a Young Family a Home

This illustrates the role of an agent in connecting buyers with suitable properties.

Relevance: Real estate professionals simplify the process for inexperienced buyers.

Step 5: Start House Hunting

With your pre-approval and priorities in hand, it’s time to view properties. Online listings, open houses, and virtual tours make this process easier than ever. Pay attention not just to the property itself, but also to the neighborhood, commute times, and long-term growth potential of the area.

Take notes and photos during visits to compare options later. Many first-time buyers find themselves surprised at how quickly houses sell, so being prepared to act fast is important.

Step 6: Make an Offer

Once you’ve found a home, you’ll need to make a written offer. Your agent can help you determine a fair price based on comparable homes in the area. The offer typically includes contingencies for financing, inspections, and appraisal.

Sellers may accept, reject, or counter your offer. Negotiation is common, and your agent plays a vital role in securing a fair deal.

Step 7: Schedule a Home Inspection

A home inspection is one of the most important safeguards for buyers. A licensed inspector evaluates the property’s condition, identifying any structural, electrical, or plumbing issues.

If major problems are found, you can renegotiate with the seller or withdraw your offer. Skipping this step can lead to costly repairs after purchase.

Home Inspector Evaluating Electrical Systems

This emphasizes the importance of catching issues before finalizing the purchase.

Relevance: Inspections protect buyers from unforeseen expenses and ensure the property is safe and habitable.

Step 8: Secure Your Mortgage

Once your offer is accepted and inspection is complete, it’s time to finalize your mortgage. This step includes locking in an interest rate and completing underwriting, where the lender verifies all your financial details.

Choosing the right mortgage type—fixed-rate, adjustable, or government-backed loans—can save you thousands over the life of the loan. First-time buyers should consult with their lender about programs designed to reduce costs.

Step 9: Closing the Deal

Closing involves signing all the necessary documents, paying closing costs, and officially transferring ownership of the property. At this stage, you’ll receive the keys to your first home.

The process can take a few hours, and your real estate agent and attorney (if applicable) will guide you through each document. Once complete, you’re officially a homeowner.

Real-World Examples of Tools That Help First-Time Buyers

Online Mortgage Calculators

Tools like mortgage calculators allow buyers to estimate monthly payments, interest, and affordability before applying for loans.

Relevance: These tools give buyers realistic expectations, preventing financial strain later.

Virtual House Tours

Virtual reality and 3D tours offered by real estate platforms let buyers explore homes without leaving their current residence.

Relevance: This technology is especially useful for busy buyers or those relocating from different cities.

Home-Buying Apps

Apps that track property listings, schedule tours, and connect directly with agents streamline the entire process.

Relevance: Centralizing resources in one app makes the journey more efficient for first-time buyers.

The Benefits of Using Technology in Home Buying

Technology has transformed the way first-time buyers approach the real estate market. Digital tools provide transparency, save time, and expand access to information.

For example, mobile apps provide instant notifications about new listings, while smart calculators adjust affordability estimates in real time. Virtual tours save hours of travel and allow buyers to shortlist homes more effectively.

The result is a smoother, less stressful buying experience where first-time homeowners feel more confident about their decisions.

Practical Use Cases

-

Young Professionals: Digital mortgage tools help them budget effectively while balancing busy careers.

-

Families Relocating: Virtual tours allow them to evaluate homes from afar before scheduling in-person visits.

-

Budget-Conscious Buyers: Online resources provide transparency on hidden costs, helping them plan realistically.

-

First-Time Buyers with Limited Knowledge: Real estate apps and agent guidance simplify jargon-heavy processes.

Frequently Asked Questions

1. How long does it take to buy a first home?

The timeline varies, but most buyers complete the process in 2 to 6 months. Factors like market conditions, loan approval, and negotiations can affect the duration.

2. How much should I save before buying my first home?

Most lenders require a down payment of 5–20% of the home’s price, plus extra funds for closing costs, inspections, and moving expenses. The more you save, the stronger your financial position.

3. Do I really need a real estate agent for my first home purchase?

While it’s possible to buy without one, a real estate agent brings expertise, negotiation skills, and protection against costly mistakes—making them highly valuable for first-time buyers.