Top Mistakes to Avoid When Applying for a Home Loan: A Complete Guide for First-Time Buyers

Top Mistakes to Avoid When Applying for a Home Loan

Applying for a home loan is one of the biggest financial decisions you will ever make. While the excitement of owning a home is undeniable, small missteps during the mortgage application process can cost you time, money, and even approval of your loan. For first-time buyers, being aware of the top mistakes to avoid when applying for a home loan can make the difference between a smooth process and a stressful setback.

This comprehensive guide explains the most common errors, offers practical solutions, highlights real-world examples, and demonstrates how technology can help streamline your home loan journey.

Not Checking Your Credit Score Early

Why Credit Matters

Your credit score is the foundation of your mortgage application. Lenders use it to assess risk, determine interest rates, and even decide whether you qualify at all. Many first-time buyers make the mistake of checking their credit only when they are ready to apply. By then, it may be too late to correct errors or improve the score.

The Fix

Check your credit score at least six months before applying. This gives you time to pay off debts, correct inaccuracies, and improve your standing. A higher credit score not only increases approval chances but can also save you thousands in interest over the life of the loan.

Ignoring Pre-Approval

Why Pre-Approval Matters

Many buyers skip pre-approval, assuming it’s optional. Without it, you risk wasting time looking at homes outside your budget or facing disappointment when an offer is rejected. Pre-approval helps you understand how much you can borrow and strengthens your position when negotiating with sellers.

The Fix

Always get pre-approved before house-hunting. It sets realistic expectations and shows sellers you are a serious buyer. Pre-approval letters often give buyers an edge in competitive markets.

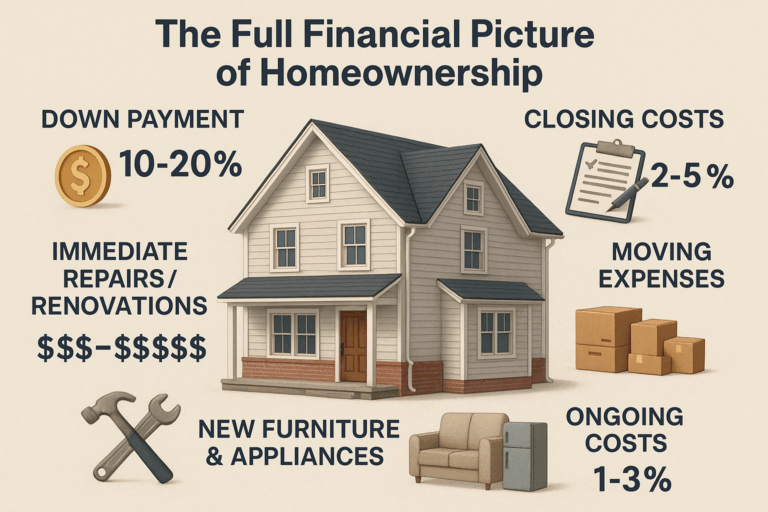

Overlooking Additional Costs

The True Price of Homeownership

Another common mistake is assuming the loan amount is the only cost. New homeowners often forget about property taxes, insurance, maintenance, and closing costs. These can add up quickly, straining your budget if unplanned.

The Fix

Build a complete cost picture before applying. Speak with financial advisors or use mortgage calculators that include taxes and insurance. Planning for hidden expenses ensures you won’t overextend yourself financially.

Changing Jobs During the Process

Why Employment Stability Matters

Insert image of the product format: Professional Packing Office Items in a Box

Lenders require steady income proof. Switching jobs in the middle of your application can delay the process or even cause denial. Even if your new job pays more, lenders may require a probation period or additional documents, complicating your approval.

The Fix

If possible, avoid major career changes until after your mortgage closes. Stability signals reliability to lenders, increasing your chances of a smooth approval.

Making Large Purchases Before Closing

How Big Buys Affect Approval

Buying a car, furniture, or expensive electronics during the mortgage process is a red flag for lenders. Large purchases increase your debt-to-income ratio and can affect your credit score, potentially disqualifying you.

The Fix

Hold off on major purchases until after closing. Prioritize financial stability during this period to keep your loan application secure.

Real-World Examples of Home Loan Mistakes

Case 1: First-Time Buyer with Credit Issues

A buyer applied for a loan without reviewing his credit report. An old, unpaid medical bill lowered his score significantly, leading to a higher interest rate. Had he checked earlier, he could have cleared the issue and saved thousands over the loan’s lifetime.

Case 2: Family Without Pre-Approval

A family found their dream home but lost the deal because another buyer had pre-approval. They wasted months looking at properties outside their actual budget. This illustrates why pre-approval is critical before starting the search.

Case 3: Buyer Making a Large Purchase

Excited to furnish their new home, a couple bought expensive furniture before closing. Their lender recalculated their debt ratio, delaying approval and jeopardizing their move-in date. A delay that could have been avoided with proper financial discipline.

Benefits of Using Technology During the Loan Process

Credit Monitoring Tools

Apps like Credit Karma and Experian provide free credit monitoring, alerts about score changes, and tips for improvement. These tools help you identify problems before applying.

Online Pre-Approval Platforms

Many banks and lenders now offer digital pre-approval tools. These platforms provide instant feedback, helping you understand your budget quickly without lengthy appointments.

Budgeting and Expense Trackers

Apps like Mint and YNAB (You Need a Budget) allow you to track spending, plan for additional costs, and avoid overspending during the loan application process.

Practical Use Cases and Problem-Solving

-

Credit Score Management – Monitoring tools prevent surprises by allowing you to address issues in advance.

-

Smarter Home Search – Pre-approval apps streamline the process, ensuring you only view homes within your budget.

-

Debt Control – Expense trackers keep you disciplined during the loan process, reducing risks of denial.

-

Time Savings – Online platforms minimize back-and-forth with lenders, making the process more efficient.

Why Avoiding These Mistakes Matters

For most people, a home loan is the largest financial commitment they will ever undertake. Mistakes during the process can lead to higher interest rates, lost opportunities, and unnecessary stress. By planning ahead, leveraging technology, and learning from real-world examples, you can ensure a smoother application and long-term financial stability.

Frequently Asked Questions

1. How long before applying for a home loan should I check my credit score?

At least six months in advance. This gives you enough time to correct errors and improve your score if necessary.

2. Is pre-approval the same as pre-qualification?

No. Pre-qualification is an informal estimate of how much you may borrow, while pre-approval involves a deeper check of your finances and carries more weight with sellers.

3. Can I still get approved if I have debt?

Yes, as long as your debt-to-income ratio is within acceptable limits. Paying down high-interest debts before applying improves your chances of approval and may result in better loan terms.